What is an adjustment in accounting

Emily Wilson

Emily Wilson An adjusting entry is simply an adjustment to your books to make your financial statements more accurately reflect your income and expenses, usually — but not always — on an accrual basis. Adjusting entries are made at the end of the accounting period. This can be at the end of the month or the end of the year.

What is an example of adjustment?

The definition of adjustment is the act of making a change, or is the change that was made. An example of an adjustment is the time that it takes for a person to become comfortable living with someone else.

What are the four types of adjustments in accounting?

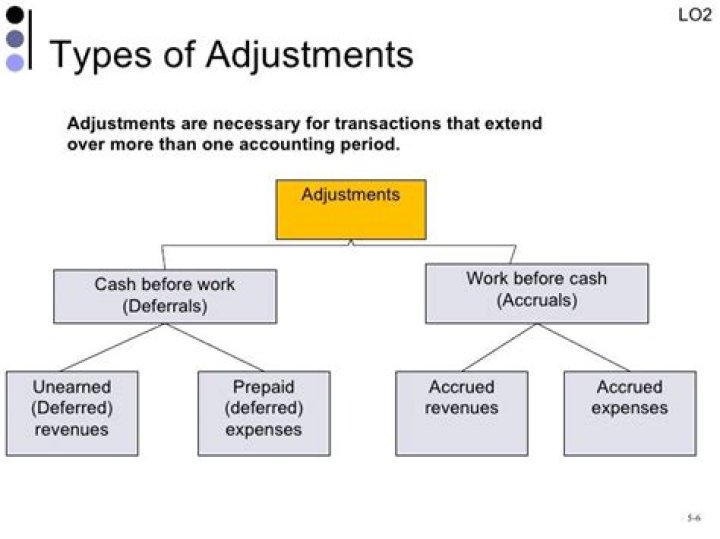

There are four types of account adjustments found in the accounting industry. They are accrued revenues, accrued expenses, deferred revenues and deferred expenses.

What is the purpose of an adjustment?

The main purpose of adjusting entries is to update the accounts to conform with the accrual concept. At the end of the accounting period, some income and expenses may have not been recorded or updated; hence, there is a need to adjust the account balances.What are 2 examples of adjustments?

- Altering the amount in a reserve account, such as the allowance for doubtful accounts or the inventory obsolescence reserve.

- Recognizing revenue that has not yet been billed.

- Deferring the recognition of revenue that has been billed but has not yet been earned.

Why do we do adjustments in accounting?

The purpose of adjusting entries is to convert cash transactions into the accrual accounting method. … The entries are made in accordance with the matching principle to match expenses to the related revenue in the same accounting period.

What is financial adjustment?

An adjusting entry is simply an adjustment to your books to make your financial statements more accurately reflect your income and expenses, usually — but not always — on an accrual basis. Adjusting entries are made at the end of the accounting period. This can be at the end of the month or the end of the year.

What are the 5 adjusting entries?

Adjustments entries fall under five categories: accrued revenues, accrued expenses, unearned revenues, prepaid expenses, and depreciation.Why do we need adjustments in accounting?

The purpose of adjusting entries is to ensure that your financial statements will reflect accurate data. If adjusting entries are not made, those statements, such as your balance sheet, profit and loss statement, (income statement) and cash flow statement will not be accurate.

What is an adjusting difference?Adjust an erroneous event with entries which reflect the different between what was recorded and what should have been recorded.

Article first time published onWhat are different types of adjusting entries?

There are three main types of adjusting entries: accruals, deferrals, and non-cash expenses. Accruals include accrued revenues and expenses. Deferrals can be prepaid expenses or deferred revenue.

How do accounting adjustments link to financial statements?

Explain how accounting adjustments link to financial statements. Accounting adjustments bring an asset or liability account balance to its correct amount. They also update related expense or revenue accounts. Every adjusting entry affects one or more income statement accounts and one or more balance sheet accounts.

What are the adjustments in final accounts?

The main adjustments that are necessary for final accounts are: (1) payments in advance by the firm, (2) payments in advance to the firm, (3) accrued expenses owed by the firm, (4) accrued receipts due to the firm, (5) bad debts, (6) provision for bad debts, (7) provision for discounts, (8) depreciation of assets, and …

What are adjustments in taxes?

Adjustments to income are expenses that reduce your total, or gross, income. You enter income adjustments directly onto Form 1040 of your tax return. … That means you benefit from adjustments to income whether you itemize deductions or take the standard deduction.

What are the main adjustments?

- Accrued expenses.

- Accrued revenues.

- Deferred expenses.

- Deferred revenues.

What is adjustment in accounting class 11?

Meaning of Adjustments in Financial Statement Every company prepares Profit & Loss Account and Trading account (also known as an income statement) and Balance Sheet statement(position statement) every financial year. … Entries passed for such financial transactions are known as adjustment entries.

What are book adjustments?

Book Adjustments means adjustments with respect to the Gross Asset Value of the Company’s assets for depreciation, depletion, amortization, and gain or loss, as computed in accordance with Section 1.704-1(b)(2)(iv)(g) of the Regulations.

What is Aje and RJE?

AJE – Adjusting Journal Entry. RJE – Reclassifying Journal Entry. FTJE – Federal Tax Journal Entry. STJE – State Tax Journal Entry.

How do you adjust overstated revenue?

If a revenue account’s debit balance is overstated, the negative adjustment is a credit entry. If an expense account’s debit balance is overstated, the negative adjustment is a credit entry. If an expense account’s credit balance is overstated, the negative adjustment is a debit entry.

What are year end adjustments?

Year-end adjustments are changes that need to be made to the balance sheet and profit and loss statement in order to ensure that the year-end reports are an accurate reflection of the company’s accounts. … Adjustments are necessary as financial reporting throughout the year will be made on an accruals basis.

What do adjusting entries affect?

Remember: ADJUSTING ENTRIES AFFECT AT LEAST ONE INCOME STATEMENT ACCOUNT AND ALSO A BALANCE SHEET ACCOUNT. THIS MEANS THAT IF AN ENTRY IS OMITTED, OR DONE IMPROPERLY, ALL OF THE FINANCIAL STATEMENTS ARE AFFECTED.

What is an adjusting journal entry in Quickbooks?

An adjusting journal entry is a type of journal entry that adjusts an account’s total balance. Accountants usually use adjusting journal entries to fix minor errors or record uncategorized transactions.

What is difference between adjustment and correction?

In short, the difference between adjusting entries and correcting entries is that adjusting entries bring financial statements into compliance with accounting frameworks, while correcting entries fix mistakes in accounting entries.

Do adjusting entries correct accounting errors?

Often, adding a journal entry (known as a “correcting entry”) will fix an accounting error. The journal entry adjusts the retained earnings (profit minus expenses) for a certain accounting period. Correcting entries are part of the accrual accounting system, which uses double-entry bookkeeping.

What kind of items are treated as adjustments?

Types of Adjusting Entries are Outstanding Expenses, Prepaid Expenses, Accrued Income, Unearned Income, Inventory. In this article, we will learn about adjusting entries, types of adjusting entries, and accounting treatment.

What is adjusted profit and loss account?

Adjusted earnings equals profits, increases in loss reserves, new business, deficiency reserves, deferred tax liabilities, and capital gains. Adjusted earnings is a helpful metric because it excludes earnings distortions such as a one-time gain or loss from the sale of an asset.

What do you mean by adjusted purchase?

Adjusted purchases means opening stock plus purchases less closing stock. Closing stock has two effects.