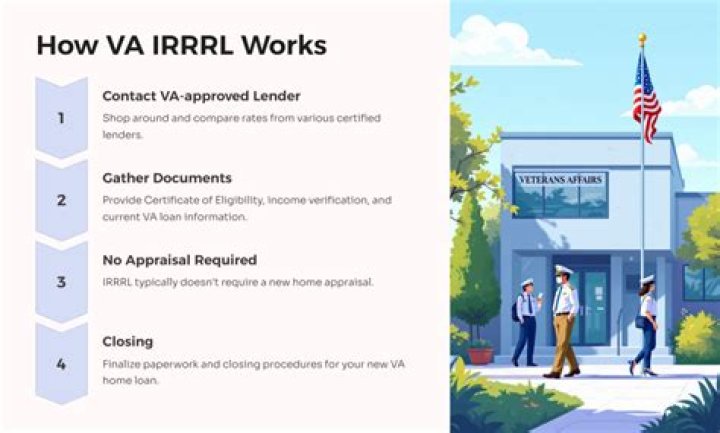

How does VA Irrrl work

Eleanor Gray

Eleanor Gray A VA Streamline Refinance may not be worth it if you’ll pay more in closing costs than you’ll save. And it won’t help you cash out your home equity. If you want to refinance with cash back – to pay for home improvements, for example – you’ll need to use the VA cash–out refinance or another cash–out loan program.

Is the VA Irrrl program worth it?

A VA Streamline Refinance may not be worth it if you’ll pay more in closing costs than you’ll save. And it won’t help you cash out your home equity. If you want to refinance with cash back – to pay for home improvements, for example – you’ll need to use the VA cash–out refinance or another cash–out loan program.

Are there closing costs with a VA Irrrl?

Closing Costs & Loan-to-Value (LTV) Unlike with a VA purchase loan, homeowners seeking an IRRRL can finance all of their closing costs, including up to two discount points and the VA Funding Fee. IRRRL borrowers who are not exempt will need to pay the VA Funding Fee.

What are the rules for a VA Irrrl?

- You are current on payments with no more than one 30–day late payment within the past year.

- Your new rate and monthly payment for the IRRRL must be lower than the previous loan’s monthly payment. …

- You must not receive any cash from the IRRRL.

What are the pros and cons of a VA Irrrl?

- Save money by lowering your interest rate.

- In most cases no appraisal is required.

- Employment proof is usually not needed.

- No dept to income verification.

- No minimum FICO score check.

- Change your loan terms.

- Faster closing times.

- Option to defer two months of mortgage payments.

Can you shorten term on VA Irrrl?

The VA allows veterans to refinance into either the same length term, a shorter term, or a longer term. The only restrictions that apply to the loan term are if you plan to go longer. The VA only allows you to add up to 10 years onto the loan, but you cannot exceed 30 years and 32 days.

Can I do a 15 year Irrrl?

Can I refinance a 30-year mortgage to a 15-year with an IRRRL? Refinancing to a 15-year mortgage is entirely possible and very common. The lifetime interest cost of a shorter loan will be less than a 30-year mortgage. However, the monthly payments on a 15-year mortgage can be significantly higher.

How long after an Irrrl can I refinance?

At least 210 days (about seven months) have passed since the first payment on the current VA loan. At least six full payments have been made on the VA loan being refinanced.Can you take cash out on a VA Irrrl?

You can’t take cash out of your home – Unlike the VA cash-out refinance, the IRRRL doesn’t allow you to receive any cash proceeds during the loan process. This is a major downside if you have a lot of home equity and you want to use it to pay down debt, pay for home improvements or reach another financial goal.

What documentation is needed for a VA Irrrl?You currently have a VA Loan. Certificate of Eligibility. Your existing VA loan is at least 6-months old. You have not been late on payments on your existing VA Loan in past 6 months OR if you’ve had it longer we can allow one 30 day late in past 12 months.

Article first time published onIs a VA Irrrl a qualified mortgage?

On May 9, 2014, the Department of Veterans Affairs (VA) issued an interim final rule defining a qualified mortgage (QM) for VA insured and guaranteed loans. … Note that while all VA IRRRLs (also known as streamlined refinance loans) are considered QM loans, not all such IRRRLs are safe harbor QM loans.

Can closing costs be rolled into a VA loan?

The VA loan allows you to include some of the closing costs into your total loan amount. The big thing is that you can roll your funding fee into the total mortgage amount. Although you’ll pay more in interest, this can help you get into a home now.

How long do you have to be Irrrl?

How soon can you do a VA IRRRL? In 2018, the Protecting Veterans from Predatory Lending Act became law. It requires a seasoning period of either 210 days from the date of the first payment or after the sixth monthly payment (whichever’s longer) before an existing VA loan can be eligible for an IRRRL.

Can I refinance twice in a year?

There’s no legal limit on the number of times you can refinance your home loan. However, mortgage lenders do have a few mortgage refinance requirements that need to be met each time you apply, and there are some special considerations to note if you want a cash-out refinance.

Can you subordinate on a VA Irrrl?

The Department of Veterans Affairs official site reminds lenders that “No loan other than the existing VA loan may be paid from the proceeds of an IRRRL.” That means that home owners with a second mortgage must request that the lender of that second mortgage allow that mortgage to be a subordinate lien so that the VA …

What is a VA Jumbo Irrrl?

It’s any loan amount that exceeds the county limit of $453,100 or $679,650 respectively. This means if you live in a high-cost county, you won’t need a jumbo loan unless you must borrow more than $679,650.

Do VA Irrrl require a pest inspection?

You still don’t need a pest inspection on a VA IRRRL refinance. But, you do need it on a standard VA refinance. This occurs when you take cash out of your VA loan or refinance from another loan type to a VA loan.

What is the VA Irrrl funding fee?

What is the VA funding fee for the VA IRRRL? Unless otherwise exempt, the VA funding fee for borrowers using the VA streamline refinance (IRRRL) is 0.5% regardless of service history or prior usage.

Is refinancing a VA loan a good idea?

When Is a VA Mortgage Refinance Worth It? … In general, lenders offer more favorable refinance rates to those with a steady income, a history of responsible credit use, and a low debt-to-income ratio. So if you have a strong credit profile and can secure low rates, this can be a worthwhile option for you.

Does VA allow subordinate financing?

The VA allows secondary borrowing under specific circumstances. … The VA puts additional restrictions on the transaction by requiring documentation about the second loan to include the amount and repayment terms.

How do I calculate maximum VA Irrrl?

– Always use VA Form 26-8923, IRRRL Worksheet, to calculate the maximum loan amount. Basically, it is the existing VA loan balance plus allowable fees and charges, including not more than 2 discount points, plus the cost of any energy efficient improvements, plus the funding fee.

Is dd214 needed for VA Irrrl?

One of the required documents for a VA IRRRL is the veterans’ DD Form 214. … You need your DD 214 to claim most of your military benefits including VA loans. Servicemen and women receive their original DD-214 at the end of their retirement or separation from the military.

Can payment increase on VA Irrrl?

Payment Increase: The P&I payment must be less than that of the existing VA loan unless: o Refinancing an ARM to a Fixed Rate; OR o The term of the new loan is less than the term of the existing VA loan. o IF the PITI increases 20% or more, refer to the PITI increase section.

How can I avoid closing costs with a VA loan?

Now, you know there are closing costs on VA loans, but what if you don’t want to or cannot bring those costs to closing? The most common way to overcome bringing these funds to closing is by seller paid closing costs and VA sales concessions. Remember, the seller is NOT required to pay the buyer’s closing costs.

Why do sellers hate VA loans?

Many sellers – and their real estate agents – don’t like VA loans because they believe these mortgages make it harder to close or more expensive for the seller. … Are less likely to close than other types of mortgages. Take ages to reach closing.

What is the VA funding fee for 2021?

2021 VA Funding Fees For Purchase And Construction Loans For cash-out or regular mortgage refinance, first-time borrowers will pay a 2.3% funding fee, while subsequent borrowers pay 3.6%.

How do you know if refinancing is worth it?

Mortgage rates have gone down So how much should mortgage rates fall before you consider whether refinancing is worth it? The traditional rule of thumb says to refinance if your rate is 1% to 2% below your current rate. Make sure to factor in your current loan term when considering refinance though.

What is the catch to refinancing?

The catch with refinancing comes in the form of “closing costs.” Closing costs are fees collected by mortgage lenders when you take out a loan, and they can be quite significant. Closing costs can run between 3–6 percent of the principal of your loan.

Does refinancing hurt credit?

Taking on new debt typically causes your credit score to dip, but because refinancing replaces an existing loan with another of roughly the same amount, its impact on your credit score is minimal.

How often is too often to refinance?

Any break–even below 24 months is generally considered a good benchmark. The bottom line is you can refinance as often as you like – as long as you’re meeting your personal financial goals. In the mortgage industry, there’s no rule that says you’re only allowed to refinance once.